How an HSA Works: A Complete Guide

Health Savings Accounts (HSAs) are an essential tool for managing healthcare costs effectively. This guide will explain how HSAs work, their benefits, contribution rules, and more, all in straightforward terms to help you understand why an HSA might be a smart choice for your financial and healthcare planning.

Get your FREE Retirement Plan Review today!

What is a Health Savings Account (HSA)?

A Health Savings Account (HSA) is a tax-advantaged savings account designed to help individuals with high-deductible health plans (HDHPs) save for medical expenses that their insurance doesn't cover. Think of an HSA as a personal savings account specifically for healthcare costs. The primary appeal of an HSA lies in its triple tax benefits: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free.

Key Features of HSAs:

Tax Advantages:

Contributions: The money you contribute to your HSA is tax-deductible, reducing your taxable income. This means you pay less in federal income taxes.

Earnings: Any interest or investment earnings on the funds in the HSA grow tax-free. You won’t pay taxes on the growth of your HSA funds.

Withdrawals: When you use HSA funds for qualified medical expenses, those withdrawals are tax-free. This makes paying for medical expenses more affordable.

Portability:

Your HSA remains with you even if you change jobs or retire. Unlike some employer-sponsored health plans, you own your HSA, and the funds roll over year after year without any expiration date. This means you can build substantial savings over time without the worry of losing your money if your employment situation changes.

Investment Opportunities:

Many HSA providers offer investment options, allowing you to grow your savings over time. You can invest in mutual funds, stocks, and other securities, similar to a retirement account. This gives you the potential to increase your HSA balance significantly, providing a larger pool of funds for future medical expenses.

How Does an HSA Work?

To open an HSA, you must be enrolled in a high-deductible health plan (HDHP). These plans have higher deductibles but lower premiums, making them suitable for those who do not expect frequent medical expenses but want coverage for major health events.

Eligibility Requirements:

Must be enrolled in an HDHP.

Cannot have other health coverage.

Cannot be enrolled in Medicare.

Cannot be claimed as a dependent on someone else's tax return.

Contribution Limits:

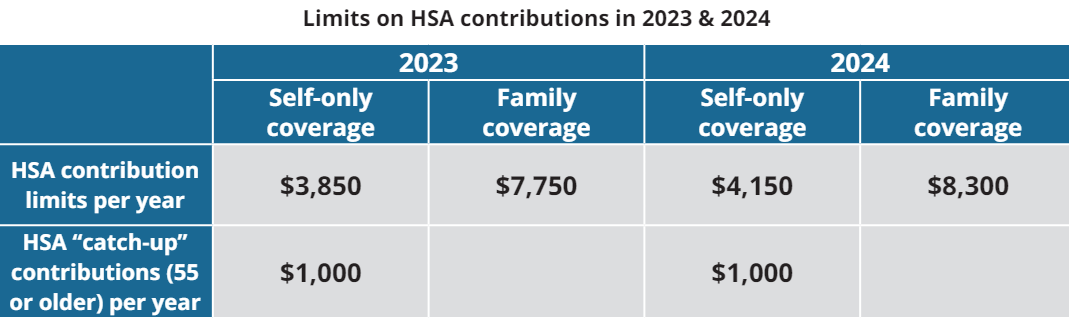

For 2024, the maximum contribution limits are:

Individual: $4,150

Family: $8,300

Catch-Up Contributions: If you are 55 or older, you can contribute an additional $1,000 annually.

Source: Healthcare.gov

Benefits of an HSA

HSAs offer a unique combination of tax advantages, long-term savings potential, and flexibility, making them an excellent choice for those with high-deductible health plans. However, they require careful planning and discipline to maximize their benefits. By understanding the pros and cons, you can make informed decisions about incorporating an HSA into your healthcare and financial strategy.

Triple Tax Advantage

Tax-Deductible Contributions: Contributions made to an HSA are not subject to federal (and possibly state) income tax. This means you can reduce your taxable income by the amount you contribute, resulting in significant tax savings each year.

Tax-Free Earnings: Interest and investment earnings on HSA funds grow tax-free. Unlike other investment accounts where you might pay taxes on the interest or dividends earned, the growth in your HSA is not taxed.

Tax-Free Withdrawals: Withdrawals for qualified medical expenses are not taxed. This feature provides a substantial financial benefit, as you can use pre-tax dollars for medical expenses, effectively reducing the cost of your healthcare.

Long-Term Savings

No Expiration: Funds in an HSA do not expire. They roll over year after year, allowing you to build significant savings over time. Unlike Flexible Spending Accounts (FSAs) that have a "use-it-or-lose-it" rule, HSA funds remain available indefinitely.

Retirement Benefits: After age 65, HSA funds can be used for non-medical expenses without a penalty, though they will be subject to income tax. This makes HSAs a flexible savings tool that can supplement retirement income, similar to a traditional IRA or 401(k).

Flexibility

Portability: Your HSA stays with you regardless of job changes. Unlike some employer-sponsored benefits that you might lose when changing jobs, an HSA is owned by you and moves with you, providing continuous coverage and savings.

Family Use: You can use HSA funds to pay for qualified medical expenses for your spouse and dependents, even if they are not covered under your HDHP. This allows you to manage family healthcare costs more effectively.

Pros and Cons of HSAs

Pros

Tax Savings: The triple tax advantage (tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified expenses) makes HSAs an excellent tool for paying for healthcare costs and saving on taxes.

Investment Growth: The ability to invest HSA funds in stocks, bonds, and mutual funds can significantly increase your savings over time, providing a robust financial resource for future medical expenses or retirement.

Long-Term Flexibility: The funds do not expire, and the account remains with you regardless of employment changes. This long-term flexibility makes HSAs a reliable savings tool.

Broad Use: HSAs can be used for a wide range of medical expenses, including those for your spouse and dependents, enhancing their utility for family healthcare planning.

Cons

High Deductible Requirement: To qualify for an HSA, you must have a high-deductible health plan (HDHP). These plans can mean higher out-of-pocket costs before insurance kicks in, which might not be suitable for everyone, particularly those with frequent medical needs.

Requires Financial Discipline: Building significant savings in an HSA requires discipline to regularly contribute and invest funds. Individuals without the ability to set aside money may not fully benefit from an HSA.

Record-Keeping: You must keep detailed records of your medical expenses and HSA withdrawals to ensure they meet IRS requirements for qualified medical expenses. This can be a burden for some account holders.

Potential Penalties: Withdrawals for non-medical expenses before age 65 incur income tax and a 20% penalty. This can be a significant drawback if funds are needed for non-medical emergencies.

Get your FREE Retirement Plan Review today!

How to Use Your HSA

Qualified Medical Expenses:

Funds from an HSA can be used for various medical expenses, including but not limited to:

Doctor visits

Prescription drugs

Dental and vision care

Hearing aids

Long-term care services

Non-Medical Use:

If you withdraw HSA funds for non-medical expenses before age 65, you will pay income tax and a 20% penalty. After 65, you can use the funds for non-medical expenses without the penalty, though you will still pay income tax.

Investing Your HSA Funds

Many people keep their HSA funds in cash, but investing part of your HSA can be a smart way to grow your savings.

Investment Strategy:

Keep a Cash Reserve: Maintain two to three years' worth of medical expenses in cash or low-risk investments.

Invest the Rest: Consider investing the remaining funds in a diversified portfolio to grow your savings over time.

Special Considerations

High-Deductible Health Plans (HDHPs):

HDHPs have higher deductibles and out-of-pocket costs but lower premiums. The minimum deductible for an HDHP in 2024 is $1,600 for individuals and $3,200 for families. The annual out-of-pocket maximum is $8,050 for self-coverage and $16,100 for families.

Contribution Rules:

Contributions can be made in cash and are vested immediately.

Contributions are limited to a specific amount each year, and any excess contributions are subject to a 6% tax.

Self-employed individuals can also contribute to an HSA if they meet the eligibility requirements.

HSA vs. Flexible Spending Account (FSA)

HSAs and FSAs both help you save for medical expenses, but they have key differences:

Ownership: HSAs are owned by the individual, while FSAs are employer-sponsored.

Rollover: HSA funds roll over year to year, while unused FSA funds are forfeited at the end of the year.

Contribution Limits: HSA contributions are higher compared to FSAs.

Common Questions About HSAs

Can I Use HSA Funds to Pay Insurance Premiums?

Generally, no. HSA funds cannot be used to pay insurance premiums except for certain circumstances, such as:

Medicare premiums for those 65 or older.

Healthcare continuation coverage (COBRA).

Health insurance while receiving unemployment compensation.

Long-term care insurance.

What Happens to My HSA If I Change Jobs?

Your HSA stays with you regardless of job changes. You can continue to use the funds for qualified medical expenses, and if you are still enrolled in an HDHP, you can continue to make contributions.

What If I Don’t Use All My HSA Funds Each Year?

Unlike FSAs, HSA funds roll over each year. Unused funds remain in your account, allowing you to build substantial savings over time.

How Can I Open an HSA?

You can open an HSA through banks, credit unions, insurance companies, and other financial institutions. Look for an HSA provider that offers low fees and investment options that suit your financial goals.

How a CERTIFIED FINANCIAL PLANNER™ Can Help You with Your HSA

Navigating the intricacies of HSAs can be complex, and this is where a CERTIFIED FINANCIAL PLANNER™ (CFP®) can be invaluable. A CFP® can help you maximize the benefits of your HSA and integrate it into your broader financial strategy.

Personalized Advice:

A CFP® provides personalized advice based on your unique financial situation and goals. They can help you determine the optimal contribution levels and investment strategies for your HSA, ensuring you make the most of your tax-advantaged savings.

Investment Guidance:

Investing your HSA funds can be a powerful way to grow your savings, but it requires a thoughtful strategy. A CFP® can guide you on how to allocate your HSA investments based on your risk tolerance, time horizon, and financial objectives.

Retirement Planning:

An HSA can be an excellent tool for retirement planning, especially since you can use the funds for non-medical expenses after age 65 without penalty. A CFP® can help you plan for healthcare costs in retirement and integrate your HSA with other retirement accounts like 401(k)s and IRAs.

Tax Optimization:

Maximizing the tax benefits of an HSA requires careful planning. A CFP® can advise you on the best ways to contribute to and withdraw from your HSA to minimize your tax liability and maximize your savings.

Coordination with Other Financial Goals:

Your HSA is just one part of your overall financial picture. A CFP® can help you coordinate your HSA with other financial goals, such as saving for a home, funding your children’s education, or planning for long-term care.

Bottom Line

Health Savings Accounts offer a unique combination of tax advantages, long-term savings potential, and flexibility, making them an excellent choice for those with high-deductible health plans. By understanding how an HSA works and leveraging its benefits, you can better manage your healthcare costs and invest in your financial future. Whether you are looking to cover routine medical expenses or save for retirement, an HSA can be a valuable tool in your financial toolkit.

Discover how a Health Savings Account (HSA) can benefit you. Visit ONE Advisory Partners today to get expert advice on integrating HSAs into your financial plan. Let us help you navigate the complexities and make the most of your healthcare investments. Contact us now to start planning for a healthier, wealthier tomorrow!

Get your FREE Retirement Plan Review today!

Reference

Employee Benefit Research Institute (EBRI). Trends in Health Savings Account Balances, Contributions, Distributions, and Investments: 2011-2021.

Spiegel, Jake and Fronstin, Paul. Projected Savings Medicare Beneficiaries Need for Health Expenses Remained High in 2022. Employee Benefit Research Institute (EBRI), February 9, 2023.

Schwab. Demystifying Medicare in Retirement.

Investopedia. High-Deductible Health Plan (HDHP).

Investopedia. Best Health Savings Account (HSA) Providers.

Internal Revenue Service (IRS). Publication 969: Health Savings Accounts and Other Tax-Favored Health Plans.

Investopedia. Pros and Cons of a Health Savings Account (HSA).