Smart Strategies to Minimize Taxes on Your Inheritance

Inheriting money or assets from a loved one can be a mixed emotional experience. While it might provide financial relief, it's essential to understand the tax implications to maximize the benefit of your inheritance. Here’s a detailed guide to help you navigate through the taxation rules and minimize your tax bill on an inheritance.

Get your FREE Retirement Plan Review today!

Types of Taxes on an Inheritance

When you inherit assets, you might encounter three types of taxes: inheritance tax, capital gains tax, income tax, and estate tax. Here’s a breakdown of each type:

Inheritance Tax

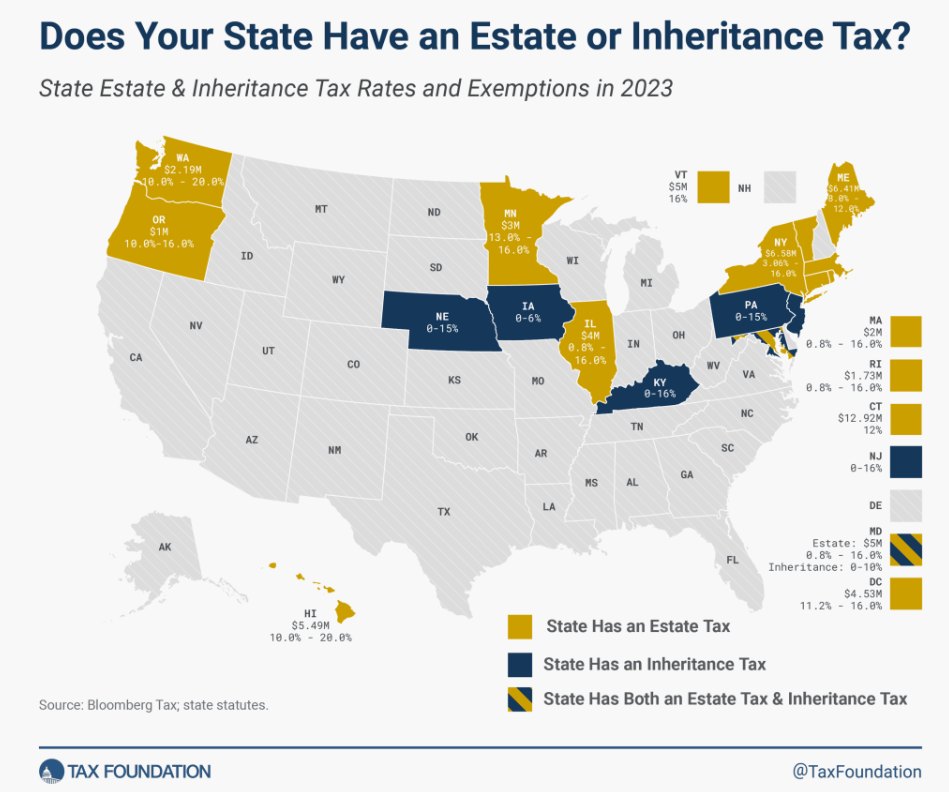

Inheritance tax depends on state laws and is imposed on the value of the assets you inherit. As of 2022, only six states in the U.S. impose an inheritance tax: Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania.

Thresholds and Rates: Each state has a threshold amount above which the tax is applied. For instance, if a state's threshold is $2 million and the inheritance tax rate is 5%, inheriting $5 million means you'll pay 5% tax on $3 million. Each state varies in its approach:

Iowa: Spouses, parents, grandparents, children, stepchildren, grandchildren, and great-grandchildren are exempt. The tax rate for others ranges from 2% to 6%. This tax will be repealed in 2025.

Kentucky: Immediate family members are exempt; other recipients face a sliding scale from 4% to 16%.

Maryland: Immediate family and charities are exempt; other recipients pay 10%.

Nebraska: Immediate family is exempt up to $100,000; others have varying exemptions with rates of 1%, 11%, and 15%.

New Jersey: Immediate family and charities are exempt; others face rates from 11% to 16%.

Pennsylvania: Spouses and minor children are exempt; others face rates of 4.5%, 12%, or 15%.

Exemptions: Generally, spouses, children, and other dependents are exempt from inheritance tax, reducing the tax burden significantly based on familial relationships.

Capital Gains Tax

Capital gains tax applies when you sell an inherited asset, like property, and is calculated based on the “stepped-up basis value.”

Stepped-Up Basis: This value is the market value of the asset at the time of the original owner’s death. For example, if a grandparent passes away and leaves you a house worth more than what they originally paid for it, the "stepped-up basis" is the house's value at the time of death. If you sell the asset for more than this value, the profit is subject to capital gains tax.

State and Federal Levels: Both state and federal taxes may apply, with rates varying based on your income. However, if you live in a state without income taxes, you won't pay capital gains tax at the state level. Capital gains taxes are often on a sliding scale based on your income level.

Income Tax

Distributions from certain tax-deferred accounts (e.g. pre-tax 401(k)s, pre-tax IRAs) are considered taxable income when distributed. Therefore, if you inherited a pre-tax 401(k) or pre-tax IRA and receive a distribution, you may have taxable income and likely will owe some additional income taxes.

Estate Tax

Estate tax is levied on the total value of the deceased person’s estate before any assets are distributed.

Federal Threshold: As of 2024, the federal estate tax threshold is $13.61 million per person. Estates exceeding this value are taxed at 40%.

State Thresholds: Twelve states and Washington, D.C. also impose estate taxes with varying thresholds, often around $1 million. For example:

Connecticut, District of Columbia, Hawaii, Illinois, Maine, Massachusetts, Maryland, New York, Oregon, Minnesota, Rhode Island, Vermont, and Washington: These states have exemptions lower than the federal threshold, making state estate taxes more common.

Maryland: Uniquely imposes both estate and inheritance taxes, creating a double tax burden for some beneficiaries.

How to Manage These Tax Implications

Here are practical steps to minimize your tax liability on an inheritance:

Manage Inheritance Tax

Use Trusts: If you live in a state with inheritance tax, consider asking the benefactor to place assets in a trust. Trusts often bypass probate and can reduce taxable amounts. Irrevocable trusts are particularly effective as they remove the assets from the estate.

Life Insurance Policies: Death benefits from life insurance are generally not taxed. Encouraging the benefactor to take out a life insurance policy can be a tax-efficient way to pass on wealth. Life insurance payouts to named beneficiaries typically avoid inheritance tax. However, life insurance products can be costly, so any tax benefit will need to be weighted against a potential tax reduction.

Gifting During Lifetime: The IRS allows up to $16,000 per year per recipient to be given as tax-free gifts. This can reduce the taxable estate if done consistently. Multiple smaller gifts can effectively reduce the estate's value over time. State laws may vary, so make sure to check with a tax or legal professional familiar with your state’s rules.

Manage Capital Gains Tax

Alternate Valuation Date: If you’re the executor, you might choose an alternate valuation date, six months after the death, which could lower the taxable value. This option is useful if the property's value decreases after the death.

Hold or Sell Strategy: Consider holding on to the inherited property until a more favorable tax situation arises or selling it in a lower income year to minimize taxes. This strategy helps in managing when the capital gains tax will be incurred.

Manage Income Tax

Retirement plans: Determine if you are inheriting tax-deferred assets such as pre-tax 401(k) or pre-tax IRA accounts.

Determine when you must take mandatory distributions: Depending upon when the deceased passed away and your relationship with the deceased, inherited pre-tax 401(k) and pre-tax IRA accounts may have to have a certain amount distributed each year as well as be distributed in a specific time-frame. Review the relevant IRS rules to make sure you are taking distributions in a timely fashion.

Timing of optional distributions: Once you understand the mandatory distributions, determine if there is an opportunity to do tax planning by timing distributions of optional distributions in years with lower taxable income or offsetting taxable distributions by increasing your pre-tax contributions to your own 401(k) or IRA (if possible).

Manage Estate Tax

Estate Planning: If your loved one’s estate is large, estate planning is crucial. This might include making use of a deceased spouse’s unused exemption, setting up trusts, making charitable donations, or leveraging gift tax exclusions. Charitable donations can significantly reduce the estate's taxable value.

Professional Advice: Consult with an estate attorney or tax professional to explore all options and ensure compliance with state and federal laws. Professional advice ensures that all potential tax-saving strategies are considered.

Understand Inheritance Taxes

Inheritance taxes are levied by some states on the recipients of inherited assets. It is important to understand the distinction between inheritance tax and estate tax:

Inheritance Tax: Paid by the recipient of the bequest. Only six states impose this tax, and it is based on the value of the inheritance and the beneficiary's relationship to the deceased. The closer the familial relationship, the higher the exemption.

Estate Tax: Paid by the estate itself before distribution of assets. This tax is imposed by both the federal government and some states. The estate pays this tax before any distributions to beneficiaries.

When the Tax Applies

The application of inheritance tax depends on:

State Laws: Only states where the deceased lived or owned property might impose an inheritance tax.

Value of the Inheritance: Inheritances must often exceed a minimum amount before tax is due. For example, Maryland exempts estates smaller than $50,000.

Relationship to the Deceased: Closer familial relationships usually enjoy higher exemptions and lower tax rates. Spouses and direct descendants often have the highest exemptions.

How to Calculate Inheritance Taxes

Inheritance tax is applied only to the portion of an inheritance that exceeds an exemption amount. Here’s how it works:

Exemption Thresholds: Each state has different thresholds. For example, in Iowa, inheritances below $25,000 are exempt.

Tax Rates: Rates range from single digits to about 18%, depending on the state and relationship to the deceased. The tax is typically progressive, increasing with the value of the inheritance.

Exemption Amount and Tax Rates

Inheritance taxes are typically applied on a sliding scale. For example, if the exemption threshold is $100,000 and you inherit $150,000, you will usually owe taxes on the $50,000 that exceeds the exemption. The tax rates usually start in the single digits and can rise to between 15% and 18%.

Example Calculation

Consider a state where the inheritance tax is applied to bequests larger than $100,000 with a tax rate of 10%. If you inherit $150,000, the calculation would be:

Amount subject to tax: $150,000 - $100,000 = $50,000

Tax owed: $50,000 x 0.10 = $5,000

Thus, your tax bill would be $5,000.

How to Minimize Inheritance Tax

Strategies to minimize exposure to inheritance tax include:

Life Insurance Policies: Life insurance death benefits are typically not subject to inheritance tax. These policies can be structured to avoid tax implications entirely. Assess whether the additional costs of the life insurance policy exceed the potential reduction inheritance tax.

Trusts: Irrevocable trusts can remove assets from your estate and control distribution after death, reducing taxable inheritance. These trusts need to be carefully structured to comply with state laws.

Federal Estate Tax

The federal estate tax applies to estates exceeding $13.61 million in 2024. The tax is levied before the estate is distributed and can range from 18% to 40%. This tax is only paid on the amount that exceeds the federal exemption.

State Estate Tax

Twelve states and Washington, D.C. impose estate taxes, with exemptions significantly lower than the federal threshold. Maryland is unique in imposing both estate and inheritance taxes. States like Connecticut and New York have lower thresholds, making it more likely for estates to be taxed at the state level.

How a Financial Advisor Can Help with Your Inheritance

Inheriting assets from a loved one can bring both financial relief and a sense of responsibility. While receiving an inheritance can be a significant boon, managing it wisely to honor your loved one’s legacy and ensure your financial stability requires careful planning. This is where a financial advisor can be invaluable. Here’s a detailed look at how a financial advisor can help you make the most of your inheritance.

Get your FREE Retirement Plan Review today!

Personalized Financial Planning

A financial advisor can create a personalized financial plan tailored to your specific circumstances and goals. This plan will take into account various aspects of your financial life, including:

Short-Term Needs: Immediate expenses such as debt repayment, emergency funds, or large purchases.

Long-Term Goals: Retirement planning, education funding for children, or investments.

Tax Strategies: Efficient ways to minimize taxes on your inheritance.

Investment Management

Inheriting a large sum of money or valuable assets can be overwhelming, especially if you are not familiar with investing. A financial advisor can:

Assess Your Risk Tolerance: Determine your comfort level with different types of investments.

Diversify Your Portfolio: Spread your investments across various asset classes to mitigate risk.

Monitor Performance: Continuously review and adjust your portfolio to align with your financial goals and market conditions.

Tax Optimization

Managing taxes on an inheritance can be complex, but financial advisors have the expertise to help you navigate these challenges:

Tax-Deferred Accounts: Advising on whether to place assets in tax-advantaged accounts such as IRAs or 401(k)s.

Gifting Strategies: Utilizing annual gift tax exclusions to reduce taxable estate size.

Capital Gains Tax Management: Providing guidance on when and how to sell inherited assets to minimize capital gains tax.

Estate Planning

A financial advisor can help you plan for the future and ensure that your assets are distributed according to your wishes:

Setting Up Trusts: Creating various types of trusts to protect assets and minimize estate taxes.

Beneficiary Designations: Ensuring that all your accounts and policies have the correct beneficiaries.

Legacy Planning: Developing a plan for charitable donations or passing wealth to future generations.

Managing Emotional Decisions

Inheritance often comes at a difficult emotional time. A financial advisor can provide an objective perspective and help you make rational decisions:

Avoiding Rash Decisions: Encouraging you to take time to consider your options and avoid impulsive spending.

Grief Support: Offering compassionate advice and understanding the emotional aspects of inheriting from a loved one.

Practical Steps to Take

When considering hiring a financial advisor to manage your inheritance, here are some practical steps to follow:

Research and Referrals: Look for advisors with good reputations, preferably those who come highly recommended by friends or family.

Check Credentials: Ensure your advisor is a CERTIFIED FINANCIAL PLANNER™ (CFP®) or has similar credentials.

Understand Fees: Be clear on how the advisor is compensated, whether through flat fees, hourly rates, or a percentage of assets under management.

Set Clear Goals: Have a clear understanding of what you want to achieve with your inheritance and communicate these goals to your advisor.

Regular Reviews: Schedule regular check-ins with your advisor to review your financial plan and make adjustments as needed.

Bottom Line

Inheriting assets can be both a blessing and a complex financial event. Taking the time to understand the various taxes involved and planning accordingly can help you preserve as much of your inheritance as possible. It’s always advisable to seek professional advice to navigate these complexities and make informed decisions.

By following these guidelines and consulting with experts, you can honor your loved one's legacy and make the most of your inheritance. If you need personalized financial advice, consider reaching out to our experienced financial advisors at ONE Advisory Partners. Our CERTIFIED FINANCIAL PLANNER™ (CFP®) professionals, with over 20 years of experience, are ready to help you navigate the complexities of inheritance and create a secure financial future.

Get your FREE Retirement Plan Review today!

Contact us today to learn how we can help you make the most of your inheritance and ensure your financial well-being.

Reference

Tax Policy Center. How Do State Estate and Inheritance Taxes Work?

Internal Revenue Service. Estate Tax.

Tax Foundation. Does Your State Have an Estate or Inheritance Tax?

Tax Foundation. Does Your State Have an Estate or Inheritance Tax?

TurboTax. What Are Inheritance Taxes?

Investopedia. Inheritance Tax: What It Is, How It's Calculated, and Who Pays It

https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-beneficiary

https://www.cpajournal.com/2023/08/09/portability-of-deceased-spousal-unused-exclusion-extended/